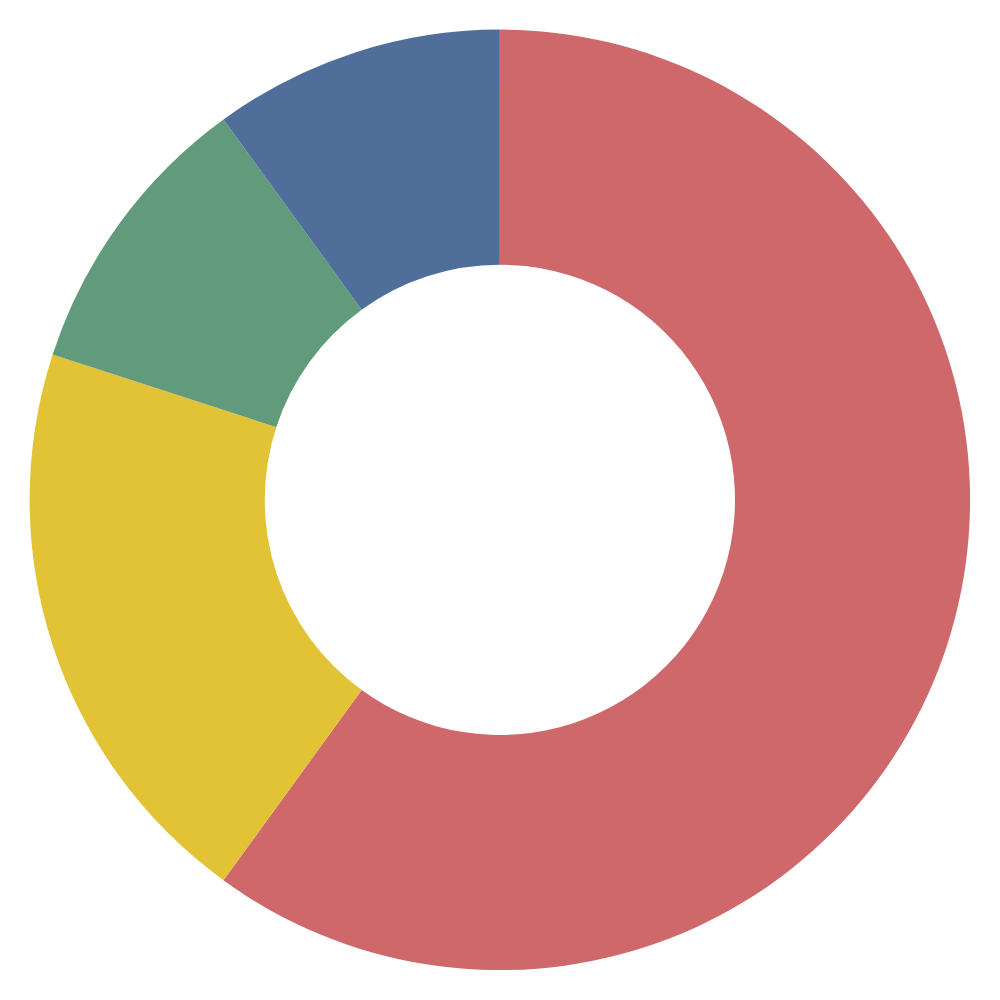

OUR METRIC

weighting

Quality lending 60%

Qualified tract presence 20%

Branch density 10%

Asset size 10%

Quality Lending

Quality lending reflects how committed a bank or credit union is to providing wealth-building loans—specifically home mortgages and small business loans. These types of loans are essential for helping families build assets and bringing more capital into local economies.

Quality Lending is measured by the total amount of first-mortgage family housing loans and small business loans outstanding, expressed as a percentage of the institution’s total assets.

By using total assets as the denominator, we also evaluate how effectively a bank is using its resources for lending—rather than parking assets in passive investments or speculative trading, as many large banks do. A higher percentage indicates a stronger focus on community investment.

Qualified Tract Presence reflects a bank or credit union’s commitment to serving low- and moderate-income (LMI) communities—based on where it chooses to place its branches. Institutions that locate branches in LMI neighborhoods are often more accessible to the people who are most underserved by traditional banking.

Qualified Tract Presence

A Qualified Census Tract (QCT) is defined by the U.S. Census Bureau as a tract where at least 50% of households earn less than 60% of the Area Median Gross Income (AMGI).

The Qualified Tract Presence score represents the percentage of a bank’s branches located within these QCTs. Nationally, about 20% of census tracts qualify.

Because most banks and credit unions are not required to disclose where their loans are made, this measure acts as a proxy for community-level lending. The logic is simple: people typically bank close to where they live—so a bank with branches in qualified tracts is more likely to be serving those communities.

While some banks do report detailed loan location data, it’s only available for a small subset of institutions and is therefore excluded from our overall scoring system.

Branch Density reflects how geographically concentrated a bank or credit union’s branches are. A tighter cluster of branches often indicates a stronger focus on local community needs—and suggests that your deposits are more likely to be reinvested in your city or neighborhood. This score also helps surface truly local banks and credit unions that may otherwise be overlooked.

Branch Density

We calculate Branch Density by first identifying the geographic center (centroid) of all an institution’s branches. Then, we measure the average distance (in miles) from each branch to that center point.

The score is calculated as:

100 − (average distance to centroid)

A score of 100 means the bank has only one branch.

Lower scores indicate that branches are spread out over a larger area.

While small or single-branch institutions often have deep local impact, Branch Density makes up only 10% of the overall score. That’s because geographic proximity doesn’t guarantee community investment—what truly matters is how well the institution serves its community through quality lending.

Asset Size

No bank should be too big to fail. Today, the 10 largest banks in the U.S. control nearly half of all banking assets—and you probably know their names. This score exists to highlight smaller, community-focused institutions that often go unnoticed but play a critical role in supporting local economies.

Let’s be honest: moving one checking account won’t hurt a mega-bank. But it can make a real difference for a smaller community bank—one that uses your deposits to fund local businesses, housing, and neighborhood growth.

This score is calculated using a non-linear formula that converts a bank’s total assets into a score between 0 and 1:

Smaller banks score closer to 1

Larger banks score closer to 0

The formula accounts for the extreme range in size—from the smallest U.S. bank (around $60,000 in assets) to the largest (over $2 trillion). A non-linear approach ensures meaningful distinctions between mid-sized institutions, not just the extremes.

While avoiding mega-banks is important, very small banks may also lack the capacity to offer impactful loans. That’s why we focus on the sweet spot—the thousands of mid-sized banks and credit unions doing responsible, community-centered work without holding outsized influence over the financial system.